Source: Probably Everything You Need To Know About Bear Markets

(WSJ) 5 Reasons to Be Scared of the Market Selloff

Investors’ anxiety has been on full display on the first day of trading for 2016

A drop by Facebook, seemingly unconnected to China’s growing pains, shows the level of anxiety. Photo: Chris Ratcliffe/Bloomberg News

Ben Eisen

Updated Jan. 4, 2016 7:09 p.m. ET

There’s nothing quite like fireworks to ring in 2016. Global markets took a diveto start the first trading session of the year, sparked by a rout in Chinese equities. A weak economic indicator in the world’s second-largest economy helped push the Shanghai Composite Index down 6.9% before trading was halted. Several markets suffered around the world. Here are some of the factors at play:

1. China Is Huge

A Chinese manufacturing gauge fell last month to 48.2, from 48.6 in November. It isn’t much of a surprise, really. Caixin Media Co.’s manufacturing purchasing-managers index, released Monday, has spat out a reading below 50, which indicates contraction, for 10 consecutive months. But it is feeding investors’ fears after a tumultuous year in Chinese markets and persistent concern about China’s economic fate. The Shanghai Composite ended last year up 9.4%, but not before a 43% crash over the summer that temporarily wiped out $5 trillion of market value. As China seeks to fuel its decelerating economy with consumption-driven businesses, rather than manufacturing, small signals are producing outsize effects in markets.

“Much of what will be dictated in the marketplace hinges on whether China is successful in arresting its decelerating rate of growth,” said Mark Luschini, chief investment strategist at Janney Montgomery Scott.

2. Real Effects

One of the biggest decliners in Monday’s selloff was the Brazilian real, which fell as low as 4.06 to the dollar before recovering to 4.04. The reason: The South American nation’s largest trading partner is China, and further weakness may push Brazil deeper into recession this year.

3. Momentum

Facebook and Google parent Alphabet Inc., which added among the most points to the S&P 500 index last year, both dropped more than 2% Monday, trailing the broader market. The fact that stocks seemingly unconnected to China’s growing pains can fall in response demonstrates the level of anxiety out there, and how many other stocks could reverse last year’s gains. Amazon.com and Netflix Inc., the two best-performing stocks in the benchmark last year, which also received analyst downgrades Monday, fell 5.8% and 3.9%, respectively.

4. Junked

The debt markets tend to flash signs of economic concern before stocks do, and that is just how bond traders ended last year. The largest high-yield bond exchange-traded fund, the iShares iBoxx $ High Yield Corporate Bond ETF fell 10% in 2015 as junk bonds marked their worst performance since 2008. Equity traders in recent weeks have finally noticed.

5. What’s Next

The CBOE Volatility Index, which tends to climb as investors become more fearful about a drop in stocks, topped 20 on Monday, a rise of 11%. Investors are finding cause for concern coming out of the first year of losses for the S&P 500 index in the past four years. Byron Wien, a vice chairman at Blackstone GroupLP, predicted in his annual list of surprises on Monday that U.S. stocks would have another down year due to weak earnings, margin pressure and “investors keeping large cash balances because of global instability.”

(The Economist) The Fed has at last raised rates. What happens next?

IT IS more than two weeks since the Federal Reserve raised interest rates for the first time in over nine years, and the world has not (yet) ended. But it is too soon to celebrate. Several central banks have tried to lift rates in recent years after long spells near zero, only to be forced to reverse course and cut them again (see chart). The outcome of America’s rate rise, whatever it may be, will help economists understand why zero exerts such a powerful gravitational pull.

Recessions strike when too many people wish to save and too few to spend. Central banks try to escape the doldrums by slashing interest rates, encouraging people to loosen their grip on their money. It is hard to lower rates much below zero, however, since people and businesses would begin to swap bank deposits for cash or other assets. So during a really nasty shock, economists agree, rates cannot go low enough to revive demand.

There is significant disagreement, however, on why economies become stuck in this quagmire for long periods. There are three main explanations. The Fed maintains that the problem stems from central-bank paralysis, either self-induced or politically imposed. That prevents the use of unconventional monetary policies such as quantitative easing—the printing of money to buy bonds. The intention of QE is to buy enough long-dated debt to lower long-term borrowing rates, thereby getting around the interest-rate floor. Once QE has generated a speedy enough recovery, senior officials at the Fed argue, there is no reason not to raise rates as in normal times.

If the Fed is right, 2016 will be a rosy year for the American economy. The central bank expects growth to accelerate and unemployment to keep falling even as it lifts rates to 1.5% or so by the end of the year. Yet markets reckon that is wildly optimistic, and that rates will remain below 1%. That is where the other two explanations come in.

The first is the “liquidity trap”, an idea which dates back to the 1930s and was dusted off when Japan sank into deflation in the late 1990s. Its proponents argue that central banks are very nearly helpless once rates drop to zero. Not even QE is much use, since banks are not short of money to lend, but of sound borrowers to lend to.

Advocates of this theory see only two routes out of the trap. The government can soak up excess savings by borrowing heavily itself and then spending to boost demand. Or the central bank can promise to tolerate much higher inflation when, in the distant future, the economy returns to health. The promise of higher-than-normal inflation in future, if believed, reduces the real, or inflation-adjusted, interest rate in the present, since money used to repay loans will be worth less than the money borrowed. Expectations of higher future inflation therefore provide the stuck economy with the sub-zero interest rates needed to escape the rut.

Governments pursued both these policies in the 1930s to escape the Depression. But when they reversed course prematurely, as America’s did in 1937, the economy suffered a nasty and immediate relapse. The liquidity-trap explanation suggests the Fed’s rate rise was ill-advised. The American economy, after all, is far from perky: it is growing much more slowly than the pre-crisis trend; inflation is barely above zero; and expectations of inflation are close to their lowest levels of the recovery. If this view is correct, the Fed will be forced by tumbling growth and inflation to reverse course in short order, or face a new recession.

Stuck in a glut

There is a third version of events, however. This narrative, which counts Larry Summers, a former treasury secretary, among its main proponents, suggests that the problem is a global glut of savings relative to attractive investment options. This glut of capital has steadily and relentlessly pushed real interest rates around the world towards zero.

The savings-investment mismatch has several causes. Dampened expectations for long-run growth, thanks to everything from ageing to reductions in capital spending enabled by new technology, are squeezing investment. At the same time soaring inequality, which concentrates income in the hands of people who tend to save, along with a hunger for safe assets in a world of massive and volatile capital flows, boosts saving. The result is a shortfall in global demand that sucks ever more of the world economy into the zero-rate trap.

Economies with the biggest piles of savings relative to investment—such as China and the euro area—export their excess capital abroad, and as a consequence run large current-account surpluses. Those surpluses drain demand from healthier economies, as consumers’ spending is redirected abroad. Low rates reduce central banks’ capacity to offset this drag, and the long-run nature of the problem means that promises to let inflation run wild in the future are less credible than ever.

This trap is an especially difficult one to escape. Fixing the global imbalance between savings and investment requires broad action right across the world economy: increased immigration to countries with ageing populations, dramatic reforms to stagnant economies and heavy borrowing by creditworthy governments. Short of that, the only options are sticking plasters, such as currency depreciation, which alleviates the domestic problem while worsening the pressure on other countries, or capital controls designed to restore monetary independence by keeping the tides of global capital at bay.

If this story is the right one, the outcome of the Fed’s first rises will seem unremarkable. Growth will weaken slightly and inflation will linger near zero, forcing the Fed to abandon plans for higher rates. Yet the implications for the global economy will be grave. In the absence of radical, co-ordinated stimulus or restrictions on the free flow of capital, ever more of the world will be drawn, indefinitely, into the zero-rate trap.

(RIA) 5 Investing Myths That Will Hurt You

In the summer of 1885 William R. Travers, prominent NYC businessman and builder of Saratoga Race Track, was vacationing in Newport, Rhode Island. He pointed out a long line of beautiful yachts tied up in the harbor. When he was informed that they all belonged to Wall Street brokers he simply asked,

“Where are their clients’ yachts?”.

When it comes to investing, there is nothing more dangerous to an individual’s future outcomes than falling prey to the many myths perpetrated on them by Wall Street. The investment business is, after all, just that – a business.

What Wall Street has learned, as the days of commission-based trading have been relegated to computerized trading, is that fee based management is a very profitable annuitized business model. The only trick is keeping individuals fully invested at all times so fees can be collected. This need has generated some of the biggest “myths”in the investment world to keep investors piling money into mutual funds, hedge funds and advisory accounts. Here are 5-myths worth thinking about.

1) Stay Invested – The Market Always Returns 10%

You have heard this one plenty. “Over the long-term” the stock market has generated a 10% annualized total return. So, just plunk your money down and you will be wealthy.

The statement is not entirely false. Since 1900, stock market appreciation plus dividends has provided investors with an AVERAGE return of 10% per year. Historically, 4%, or 40% of the total return, came from dividends alone. The other 60% came from capital appreciation that averaged 6% and equated to the long-term growth rate of the economy.

However, there are several fallacies with the notion that the markets long-term will compound 10% annually.

1) The market does not return 10% every year. There are many years where market returns have been sharply higher and significantly lower.

2) The analysis does not include the real world effects of inflation, taxes, fees, and other expenses that subtract from total returns over the long-term.

3) You don’t have 144 years to invest and save.

The chart below shows what happens to a $1000 investment from 1871 to present including the effects of inflation, taxes, and fees. (Assumptions: I have used a 15% tax rate on years the portfolio advanced in value, CPI as the benchmark for inflation and a 1% annual expense ratio. In reality, all of these assumptions are quite likely on the low side.)

As you can see, there is a dramatic difference in outcomes over the long-term.

From 1871 to present the total nominal return was 9.07% versus just 6.86% on a “real” basis. While the percentages may not seem like much, over such a long period the ending value of the original $1000 investment was lower by an astounding $260 million dollars.

Importantly, as stated previously, and as I will discuss more in a moment, the return that investors receive from the financial markets is more dependent on the “WHEN” you begin investing.

2) I Can Beat/Outperform The Stock Market

No, you can’t and the data proves it.

Dalbar recently released their 21st annual Quantitative Analysis Of Investor Behavior study which continues to show just how poorly investors perform relative to market benchmarks over time and the reasons for that under performance.

It is important to note that it is impossible for an investor to consistently “beat” an index over long periods of timedue to the impact of taxes, trading costs, and fees. Furthermore, there are internal dynamics of an index that affect long term performance which do not apply to an actual portfolio such as share repurchases, substitution, and replacement effects.

However, even the issues shown above do not fully account for the underperformance of investors over time. The key findings of the study show that:

- In 2014, the average equity mutual fund investor underperformed the S&P 500 by a wide margin of 8.19%.The broader market return was more than double the average equity mutual fund investor’s return. (13.69% vs. 5.50%).

- In 2014, the average fixed income mutual fund investor underperformed the Barclays Aggregate Bond Index by a margin of 4.81%. The broader bond market returned over five times that of the average fixed income mutual fund investor. (5.97% vs. 1.16%).

- Retention rates are

- slightly higher than the previous year for equity funds and

- increased by almost 6-months for fixed income funds after dropping by almost a year in 2013.

- In 2014, the 20-year annualized S&P return was 9.85% while the 20-year annualized return for the average equity mutual fund investor was only 5.19%, a gap of 4.66%.

- In 8 out of 12 months, investors guessed right about the market direction the following month. Despite “guessing right” 67% of the time in 2014, the average mutual fund investor was not able to come close to beating the marketbased on the actual volume of buying and selling at the right times.

Most importantly, despite what Wall Street and advisors want you to believe, 50% of the shortfall was directly attributable to psychology – both theirs and yours. The other 50% came down to lack of capital to invest.

So, the next time you hear the mainstream media chastise investors for not beating some random benchmark index, just realize they didn’t either.

3) Your Financial Plan Says You Will Be Just Fine

One the biggest mistakes that investors make are in the planning assumptions for their retirement. As I discussed previously:

“There is a massive difference between compounded returns and real returns as shown. The assumption is that an investment is made in 1965 at the age of 20. In 2000, the individual is now 55 and just 10 years from retirement. The S&P index is actual through 2014 and then projected through age 100 using historical volatility and market cycles as a precedent for future returns.”

“While the historical AVERAGE return is 7% for both series, the shortfall between ‘compounded’ returns and ‘actual’ returns is significant. That deficit is compounded further when you begin to add in the impact of fees, taxes and inflation over the given time frame.

The single biggest mistake made in financial planning is NOT to include variable rates of return in your planning process.”

So, look at your financial plan projections. If they are a smooth curve upwards, you are going to be very disappointed.

4) If You’re Not In, You’re Missing Out

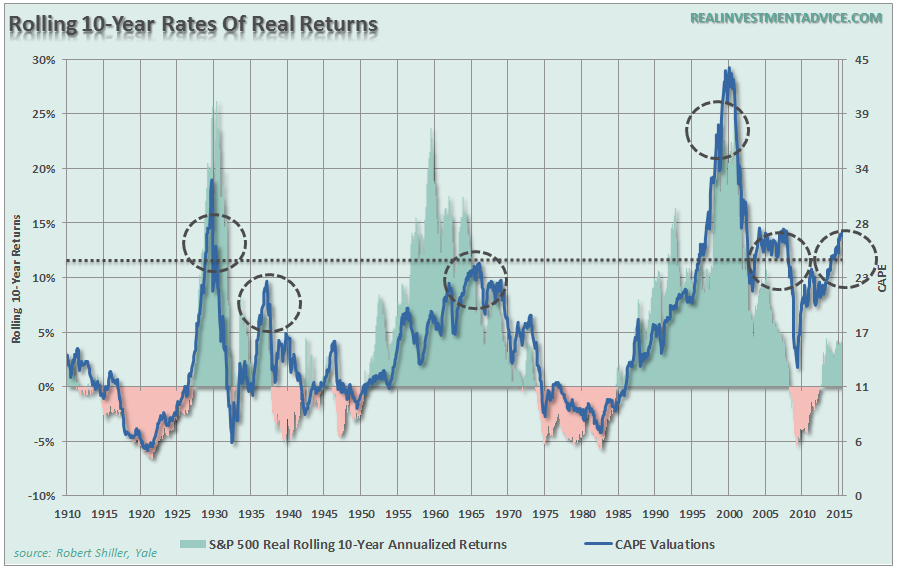

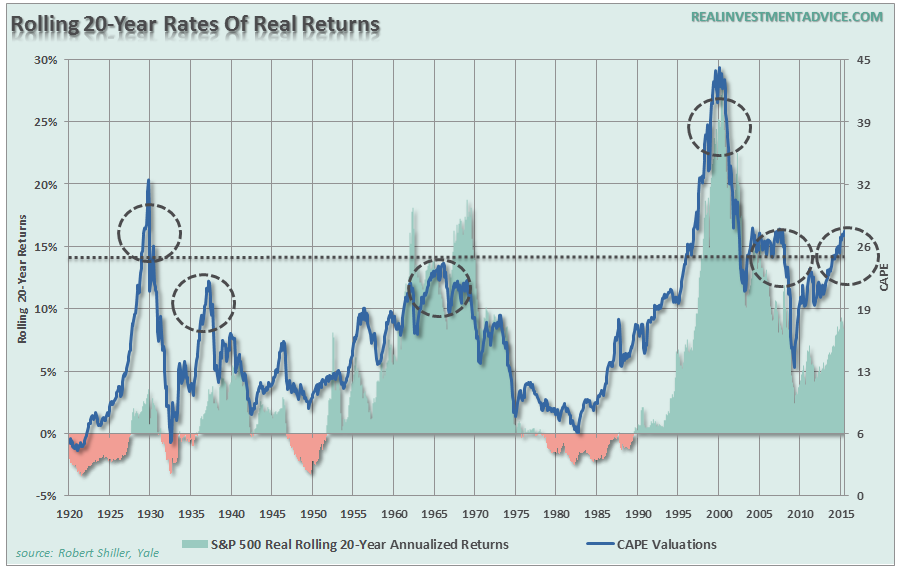

It is often stated that you should remain invested in the markets at all times because there has NEVER been a 10-year period that has produced negative returns for investors. That is simply not true.

Okay, but over 20-years investors have never lost money, right? Not really.

There are two important points to take away from the data. First, is that there are several periods throughout history where market returns were not only low, but negative. Secondly, the periods of low returns follow periods of excessive market valuations.

In other words, it is vital to understand the “WHEN” you begin investing that affects your eventual outcome.

The chart below compares Shiller’s 10-year CAPE to 20-year actual forward returns from the S&P 500.

From current levels history suggests returns to investors over the next 20-years will likely be lower than higher. We can also prove this mathematically as well as shown.

From current levels history suggests returns to investors over the next 20-years will likely be lower than higher. We can also prove this mathematically as well as shown.

Capital gains from markets are primarily a function of market capitalization, nominal economic growth plus the dividend yield. Using John Hussman’s formula we can mathematically calculate returns over the next 10-year periodas follows:

(1+nominal GDP growth)*(normal market cap to GDP ratio / actual market cap to GDP ratio)^(1/10)-1

Therefore, IF we assume that GDP could maintain 4% annualized growth in the future, with no recessions, AND IF current market cap/GDP stays flat at 1.25, AND IF the current dividend yield of roughly 2% remains, we get forward returns of:

(1.04)*(.8/1.25)^(1/10)-1+.02 = 1.5%

Regardless, there are a “whole lotta ifs” in that assumption. More importantly, if we assume that inflation remains stagnant at 2%, as the Fed hopes, this would mean a real rate of return of -0.5%. This is certainly not what investors are hoping for.

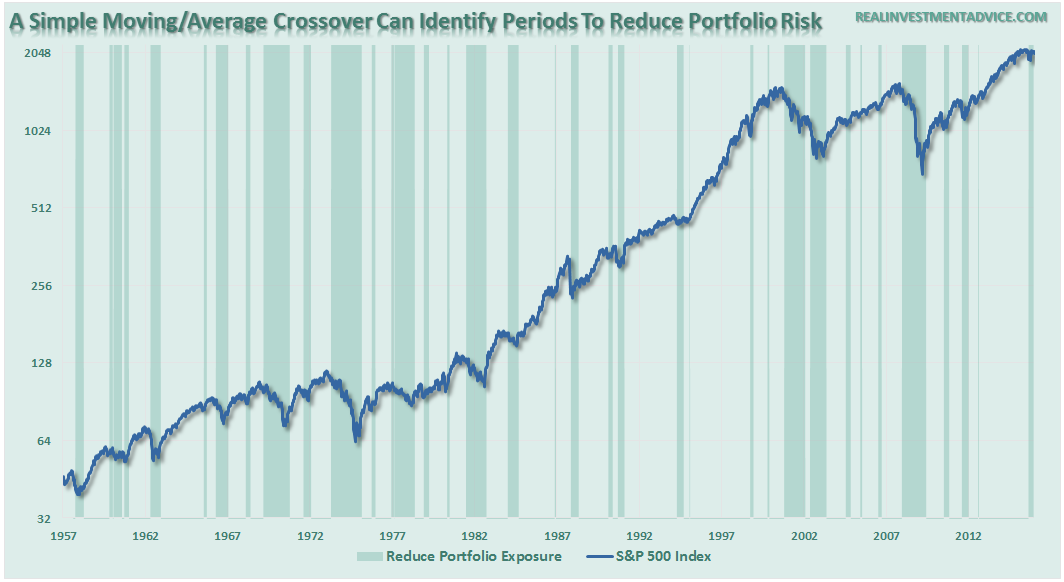

5) You Can’t Time The Market – Just Buy And Hold

There are no great investors of our time that “buy and hold” investments. Even the great Warren Buffett occasionally sells investments. Real investors buy when they see value, and sell when value no longer exists.

While there are many sophisticated methods of handling risk within a portfolio, even using a basic method of price analysis, such as a moving average crossover, can be a valuable tool over the long term holding periods. Will such a method ALWAYS be right? Absolutely not. However, will such a method keep you from losing large amounts of capital? Absolutely.

The chart below shows a simple moving average crossover study. The actual moving averages used are not relevant, but what is clear is that using a basic form of price movement analysis can provide a useful identification of periods when portfolio risk should be REDUCED.

Importantly, I did not say risk should be eliminated; just reduced.

Again, I am not implying, suggesting or stating that such signals mean going 100% to cash. What I am suggesting is that when “sell signals” are given that is the time when individuals should perform some basic portfolio risk management such as:

- Trim back winning positions to original portfolio weights: Investment Rule: Let Winners Run

- Sell positions that simply are not working (if the position was not working in a rising market, it likely won’t in a declining market.) Investment Rule: Cut Losers Short

- Hold the cash raised from these activities until the next buying opportunity occurs. Investment Rule: Buy Low

The reason that portfolio risk management is so crucial is that it is not “missing the 10-best days” that is important; it is “missing the 10-worst days.” The chart below shows the comparison of $100,000 invested in the S&P 500 Index (log scale base 2) and the return when adjusted for missing the 10 best and worst days.

Clearly, avoiding major drawdowns in the market is key to long-term investment success. If I am not spending the bulk of my time making up previous losses in my portfolio, I spend more time growing my invested dollars towards my long term goals.

Chasing A Unicorn

There are many half-truths perpetrated on individuals by Wall Street to sell product, gain assets, etc. However, if individuals took a moment to think about it, the illogic of many of these arguments are readily apparent.

Chasing an arbitrary index that is 100% invested in the equity market requires you to take on far more risk that you realize. Two massive bear markets over the last decade have left many individuals further away from retirement than they ever imagined. Furthermore, all investors lost something far more valuable than money – the TIME needed to achieve their goal.

To win the long-term investing game, your portfolio should be built around the things that matter most to you.

- Capital preservation

- A rate of return sufficient to keep pace with the rate of inflation.

- Expectations based on realistic objectives. (The market does not compound at 8%, 6% or 4% every year, losses matter)

- Higher rates of return require an exponential increase in the underlying risk profile. This tends to not work out well.

- You can replace lost capital – but you can’t replace lost time. Time is a precious commodity that you cannot afford to waste.

- Portfolios are time-frame specific. If you have a 5-years to retirement but build a portfolio with a 20-year time horizon (taking on more risk) the results will likely be disastrous.

The index is a mythical creature, like the Unicorn, and chasing it has historically led to disappointment. Investing is not a competition, and there are horrid consequences for treating it as such.

So, the next time a financial professional encourages you to just “buy and hold” for the long-term, maybe you should question just who’s “yacht” are you buying?

(FT) Junk bond market tests nervous investors

Debt burden of high-yield companies at highest level since 1998

December 16, 2015by: Eric Platt

Investors are discovering why high-yield bonds are also called “junk”.

After years of ignoring the low credit ratings and indebted balance sheets of companies within the junk bond sector, a wave of redemptions for three funds — forcing two to shutter in the past week — has triggered a frisson across the US fixed income market.

With the US Federal Reserve expected to nudge overnight borrowing costs up from near zero on Wednesday, the $1.3tn junk bond market has already begun counting the cost of the easy money era.

While much of the pain reflects heavily indebted gas drillers and miners hit hard by a collapse in commodity-based revenues, the pain in junk has spread to other sectors, suggesting that years of booming debt sales are catching up with companies and investors.

Bonnie Baha, head of global developed credit at DoubleLine Capital, says that the closure of funds managed by Third Avenue and Lucidus, and the decision to bar redemptions from a Stone Lion credit fund, sparked a reassessment of risk by investors.

“It brings back bad memories of 2008 all over again and that’s what really has been fuelling this [sell-off],” Ms Baha says. “Defaults are ticking up. Energy is leading the way but now it’s starting to spread to other sectors. It’s not just an energy or metals and mining issue.”

Indeed, the price of bonds, which move inversely to yield, issued by companies in the pharmaceuticals, media, telecoms, semiconductor and retail industries have slid in the final months of the year. That has intensified the pressure on bond portfolios and also popular exchange traded funds that track the sector,such as HYG and JNK.

The broad high-yield market is currently on course for its first negative year of performance since 2008, while Triple C-rated bonds, the most speculative rated area of junk, are yielding above 18 per cent.

Years of low interest rates spurred investors to seek returns beyond investment-grade corporate debt, with triple C debt yields falling below 8 per cent at the height of the credit boom. That duly spurred a rise in leverage as US companies locked in cheap borrowing costs, a metric that now has the attention of investors.

The debt burden of high-yield companies has risen to 6.9 times trailing 12-month earnings, the highest level since at least 1998, according to BofA Merrill Lynch. Excluding the energy sector, leverage has reached levels last touched in 2001.

David Tesher, an analyst at Standard & Poor’s, warns that the lowest-rated groups may be finding it increasingly “challenging” to tap new buyers for their debt, an issue as maturities begin to mount in the next several years.

“Credit risk is rising, in our view, and although any deterioration is still likely to be manageable, we expect companies’ credit quality to take more hits in the year ahead,” says Mr Tesher.

Against that backdrop, investment managers worry that they will be unable to sell lower-rated and less liquid bonds if there is a spike in mutual fund outflows. Investors were given a test of that scenario last week, when high-yield bond funds were hit with $3.5bn in withdrawals, the greatest redemption in 70 weeks, according to Lipper.

Trading volumes for junk ETFs have soared to record levels during the recent market sell-off, as investors have also cut their exposure to the sector, compounding the selling of bonds.

Market illiquidity became increasingly evident in November, with trading concentrated in more liquid names. The top 20 per cent of bonds in Standard & Poor’s US double B rated index accounted for nearly two-thirds of all trading last month. Trading in triple C-rated debt has become even more concentrated.

The fear thus remains of a widespread withdrawal from credit markets by retail investors who have piled into mutual funds offering attractive income, either in response to losses or as a reaction to restrictions on withdrawals by other funds.

“Recent weakness in higher-quality junk names in parallel with mutual fund outflows and illiquidity is also disconcerting, because this may be a preview to investors of how the credit cycle ultimately ends,” says Matthew Mish, a strategist with UBS.

A common refrain among hedge fund investors is that while there are real problems for businesses hit by the collapse in commodity prices — “there’s a bunch of people that need to default and are just holding on”, said one — the credit cycle overall is yet to turn.

Some strategists and investors have begun to question how much further bond prices could fall before finding a bottom. UBS notes that the number of call options on BlackRock’s HYG have been steadily rising, which indicates “investors positioning for a rebound in high yield”.

Indeed, some see value in the market.

Sir Michael Hintze, founder of CQS, a London-based credit-focused asset manager with about $12.5bn of assets under management, said that “recent liquidity-related credit market dislocations create opportunity for long-term investors”, provided they can weather volatility in prices day to day.

But not everyone is ready to step in.

“I would want this to settle down,” Ms Baha says. “Buying on the dips has rewarded investors in the cycle this far, but things are different now.”

(ValueWalk) Implications Of A Fed Funds Rate Hike On Asian Securities

The prospect of a higher U.S. federal funds rate can make U.S. cash and short duration Treasurys look more attractive vs. risky assets. The effect of higher U.S. short rates is felt across all asset classes, regardless of the pattern of cash flows or currency of denomination. We can expect some market reallocation out of risky assets and into risk-free assets. But why does the market seem to fear a wholesale shift out of risky assets and why might that view be unjustified? This month, we examine the ways in which an initial rate change impulse in the U.S. could affect security values in the U.S. and Asia.

A Framework for Considering the Effects of a U.S. Rate Hike on the Yield Curve

All else equal, a higher U.S. federal funds rate makes both bonds and equities look less attractive, but all else is rarely equal.

The fear of a rate hike is powered by the tacit assumption that rates along the entire yield curve will rise in tandem. Only such a parallel upward shift would raise discount rates on all cash flows from risky assets (e.g. equities and corporate bonds). Consequently, the present value of those assets would decline, if cash flows stay the same.

Importantly, the Federal Reserve holds sway over only short-term rates through its setting of the federal funds rate. This policy rate may be affected more by Federal Open Market Committee assessments of economic growth than by inflation.

Moreover, this short rate is a weak lever on longer rates. Rates at longer maturities embed the compounded effect of expected future real rates, expected inflation and a term risk premium that captures the volatility of these factors. Market anticipation of higher future inflation, or the possibility of inflation surprises, will be expressed as higher long-term interest rates. The Fed’s credibility anchors these market expectations, and the loss of that credibility is perhaps the biggest risk to long-term rates.

In rate hike cycles over the past 20 years, Fed credibility may have been enhanced by the very act of raising rates in the first place. One indication is in the flattening of the U.S. yield curve. In each cycle, short rates rose more than long rates. Interestingly, in two of the past four hike cycles, the longer part of the curve (10-year to 30-year) declined in yield.

A parallel shift in the yield curve is as rare as receiving the equity market’s long-term average annual return in any single year. Most likely, a future federal funds rate hike will not translate into higher rates all along the curve.

As seen in Figure 1, only the 1994 rate hike cycle saw an upward shift in the entire yield curve, yet yields at longer maturities rose less than those at the front end.

This small sample of rate hike cycles indicates that at the very least, it is possible for long-term rates to decline following a rate hike. Once the Fed takes the first step to dampen inflation, expected inflation all along the yield curve declines. This effect can cause nominal yields to decline at longer maturities when the compounded effects of lower expected inflation overtake higher expected short rates.

What Happened After the Previous Rate Hike Cycle?

Do risky assets sell off following a federal funds rate hike? To ground the discussion, let’s look at Asian sovereign bond returns (in USD terms) during the last federal funds rate hike cycle. In June 2004, the Fed embarked on the first of 17 rate hikes, staged in increments of 25 basis points (0.25%). By the time the cycle reversed into a rate cut cycle in August 2007, Asian bonds had generated a return of 27.8% (8.1% annualized).1

Figure 2 shows the steady march forward of Asian bonds through the last hike cycle.

Asian equities also rallied (33.2% annualized for the MSCI AC Asia ex Japan Index) as did the S&P 500 Index (10.4% annualized). Even intermediate U.S. Treasurys generated a 3.7% annualized return over that period.2

And Currencies?

The standard narrative is that a U.S. rate hike draws investors to the U.S. because of higher rates on dollar deposits. Alternatively, maybe a rate hike ratifies a view that the economy is on the path to sustained growth, boding well for U.S. equities. Then, the liquid and open U.S. capital markets absorb international investments, increasing demand for the dollar, and hurting Asian currencies.

Let’s look at the historical record in Figure 3. The June 1994 experience shows relatively stable Asian currencies leading up to the hike, and strengthening in aggregate after the start of the hike.

From the start of the 1994 hike cycle until the beginning of the tightening cycle, Asian currencies gained 3.7% on average. Asian currencies were not hurt either in the 2004–2006 hiking cycle, when they gained 12.4% on average.

Higher returns on Asian bonds (vs. lower yielding U.S. Treasurys) were enhanced, not negated, by currency movements. Asian local bond total return outperformance (coupon + price return + currency appreciation) occurred during a 425 basis point (4.25%) rise in U.S. federal funds over the 2004–2006 cycle.

Double Duration of Asian Bonds

Asian local currency bonds are sensitive to changes in both global and local rates. Sovereign bonds issued by more globally integrated countries should be expected to be more sensitive to changes in global rates. That’s the theory, but in practice, sovereign bond sensitivity to global rates (with U.S. rates being the proxy for global rates in this discussion) is time varying. In many cases, local rates evolution is completely disconnected from whatever is happening in the U.S., Europe, or Japan.

Historically, Asian local currency bonds have been more sensitive to the particulars of their national economies and monetary policies. In June 2005, one year after the U.S. started the rate hike cycle, the ENTIRE Korean yield curve had shifted DOWN 40–55 basis points (0.40–0.55%). That occurred in the context of a 225 basis points (2.25%) rise in U.S. federal funds over that period.

The Korean capital markets are relatively well-integrated, so a 3% price rise in the Korean 10-year Treasury bond may have surprised pundits who assumed that developed Asia bonds moved in lockstep with U.S. federal funds. It may have surprised them even more to see the 21% total return of that bond (price + coupon + currency return).

A rise in the U.S. short rate does not necessarily result in higher rates anywhere along an Asian yield curve. Even the U.S. Treasury curve does not move in lockstep with the U.S. short rate—the 10-year U.S. Treasury fell 70 basis points (0.70%) in yield in the first 12 months of the 2004–2006 cycle.

Non-USD sovereign bonds have both global duration and local currency duration. Asian bond sensitivity to changes in global rates varies. It is higher when Asian business and credit cycles are in sync with global cycles. A synchronized global recovery, for instance, would raise real rate and inflation pressures everywhere, including Asia.

(Bloomberg) Bill Gross’ Math on Junk Bonds Is Right

Can ETFs Be Blamed for the Junk Bond Rout?

Bill Gross says the selloff in junk bonds is starting to make them look cheap compared with stocks. Going by one widely followed measure, it’s true.

Amid an almost 6 percent selloff in high-yield debt this year, speculative-grade credit is yielding 3.52 percentage points more than stocks in the Standard & Poor’s 500 Index are earning — the widest spread since 2010, according to data compiled by Bloomberg. Since the start of the 6 1/2-year bull market, junk securities have held an advantage of less than half that — 1.36 percent — over equity counterparts, the data show.

Speaking in an interview with CNBC on Monday, Gross, the manager of the $1.3 billion Janus Global Unconstrained Bond Fund, said the junk selloff has made this a “perfect time” to take advantage of an “illiquidity discount.”

“The junk market is attractive,” said John Manley, who helps oversee about $233 billion as chief equity strategist for Wells Fargo Funds Management in New York. “The selloff tells me that people are particularly worried about some sort of crisis or meltdown. But the more people worry, the less likely it is to happen, so some investors are viewing this as an ideal entry point.”

In the last 20 years, there have been two extended stretches during which junk bonds have held a large advantage on a yield/earnings yield basis — from December 1996 to August 2003, and from December 2007 to February 2010. In both occasions, the Bank of America Merrill Lynch U.S. High Yield Index outperformed the S&P 500 by more than 1.3 percentage points in the following three months, Bloomberg data show.

The recent selloff in high-yield bonds has hit equity exchange-traded funds linked to the securities, including the SPDR Barclays High Yield Bond ETF and the iShares iBoxx $ High Yield Corporate Bond ETF, which both fell 5.1 percent from Dec. 2 through Dec. 14. Each rebounded more than 1.1 percent at 4 p.m. in New York on Tuesday.

The decline coincided with travails in at least three funds in recent days. Lucidus Capital Partners, founded in 2009 by former employees of Bruce Kovner’s Caxton Associates, said Monday it had liquidated its portfolio and plans to return the $900 million it has under management to investors next month. Funds run by Third Avenue Management and Stone Lion Capital Partners have stopped returning cash to investors, after clients sought to pull too much money.

“This is the perfect time in terms of an illiquidity discount for what are known as closed-end funds,” Newport Beach, California-based Gross said in the interview with CNBC. “It’s like the pelicans in Newport Beach. They’re just diving down and picking out those fish. It’s just loaded with bargains.”

(WP) Larry Summers: What the Federal Reserve got wrong, and what it should do next

By Lawrence H. Summers December 15 at 7:56 AM

The Federal Reserve building in Washington September 1, 2015. Central bankers from around the world are telling their American counterparts that they are ready for a U.S. interest rate hike and would prefer that the Federal Reserve make the move without further ado. REUTERS/Kevin Lamarque

Lawrence H. Summers, the Charles W. Eliot university professor at Harvard, is a former treasury secretary and director of the National Economic Council in the White House. He is writing occasional posts, to be featured on Wonkblog, about issues of national and international economics and policymaking.

The Federal Reserve meets this week and has strongly signaled that it will raise rates. Given the strength of the signals that have been sent, it would becredibility destroying not to carry through with the rate increase, so there is no interesting discussion to be had about what should be done on Wednesday.

There is an interesting counterfactual discussion to be had. Should a rate increase have been so clearly signaled? If rates are in fact going to be increased, the answer is almost certainly yes. The Fed has done a good job of guiding expectations toward a rate increase while generating little trauma in markets. Assuming that the language surrounding the rate increase on Wednesday is in line with what the market expects, I would be surprised if there are major market gyrations after the Fed statement.

But was it right to move at this juncture? This requires weighing relative risks. A decision to keep rates at zero would have taken several risks. First, since monetary policy acts only with a lag, failure to raise rates would risk an overheating economy and an acceleration of inflation, possibly necessitating a sharp and destabilizing hike in rates later. Second, keeping rates at zero would risk encouraging financial instability, particularly if there became a perception that the Fed would never raise rates. Third, keeping rates at zero leaves the Fed with less room to lower rates in response to problems than it would have if it increased rates.

Finally, perhaps zero rates have adverse economic effects. Perhaps economic actors take the continuation of zero rates as evidence that the Fed is worried and so they should be as well. Some believe that zero rates are a sign of pathology, and we no longer have a pathological economy, and so no longer should have zero rates. Or perhaps there is a fear that when rates go up, something catastrophic will happen, and this source of uncertainty can only be removed by raising rates.

These arguments do not seem hugely compelling to me. Inflation is running well below 2 percent and there is not yet much evidence of acceleration. Decades of experience teaches that the Phillips curve can shift dramatically so reasoning from the unemployment rate to inflation is problematic. Declining prices of oiland other commodities suggest inflation expectations may actually decline. Furthermore, if one believes that productivity is understated by official statistics one has to as a matter of logic believe that inflation is overstated. I have recently argued that this is quite likely the case given the rising importance of sectors like health care where quality is difficult to measure.

Even if one assumes that inflation could reach 2.5 percent, this is not an immense problem. There is no convincing evidence that economies perform worse with inflation marginally above 2 percent than at 2 percent. Then there is the question of whether it is better to target the annual rate of inflation or the price level. On the latter standard, it is relevant that inflation over any multiyear interval would still have averaged less than 2 percent. And I am not sure why bringing down inflation would be so difficult if that were desired especially given that it would surely take a long time for expectations to become unanchored towards the high side of 2 percent.

It seems to me looking at a year when the stock market has gone down a bit, credit spreads have widened substantially, and the dollar has been very strong, it is hard to say that now is the time to fire a shot across the bow of financial euphoria. Looking especially at emerging markets, I would judge that under-confidence and excessive risk aversion are a greater threat over the next several years than some kind of financial euphoria.

The Fed does not have special information on where the economy is going, and I find it highly implausible that its not acting would scare market participants if it explained its decision making. Given the now large body of research suggestingsubstantial declines in neutral real rates, it is an anachronism to believe that zero rates are only appropriate in pathological economies.

A very important recent study from two Bank of England economists suggests that on a global basis neutral real rates are unlikely to rise much if at all in the next few years. As I noted in yesterday, the “temporary headwinds” interpretation of low neutral real rates has been wrong for the last few years and is not hugely plausible as a basis for predicting the next few. Historically, volatility has been a bit higher for stocks and for the dollar and a bit lower for bonds after the Fed starts hiking than immediately before so, I’m not sure of the basis for the belief that “getting it over with” would reduce uncertainty.

Finally, the reload the cannon argument seems to me entirely specious. I know of no economic model where raising the average level of rates over the next few years raises the average level of output. Contractionary policy is contractionary, and if there is a risk of a slowdown or recession in the next few years, that is surely an argument against contractionary policy.

What about the risk of raising rates? Certainly the risks of exacerbating financial instability or hitting the brakes when the economy is slowing look much less serious than they did in September. Nonetheless, growth in the second half of 2015 may well come in at less than 2 percent. There is certainly a real risk that slow speed becomes stall speed becomes recession. On average, mature recoveries like the present one last less than an additional 3 years. And given how low rates are and the political aversion to the use of fiscal policy, a substantial slowdown could have very severe consequences. It is important to recognize in this regard that once the decline in neutral real rates is recognized, policy is much less accommodative than is often supposed. Indeed on some measures policy rates now are above neutral.

There is also the risk that inflation expectations start to anchor below 2 percent. This will happen if economic actors conclude as they reasonably can from what they are hearing that the Fed will cap inflation at 2 percent but allow it to fall below 2 percent in periods of economic slack. If anything, the picture coming from survey measures of expectations, from the indexed bond market and from inflation swaps suggests that inflation is expected to remain below 2 percent for a decade. If projections were conditioned on the Fed’s intended path of monetary policy rather than what the market expects, they would be even lower. And if account was taken of inflation mismeasurement they would be lower still.

All of the argument about appropriate inflation targeting in recent years has focused not on whether 2 percent is too high, but on whether it is too low a target. I am not yet ready to abandon a 2 percent target, but wage rigidity and zero lower bound on interest rate considerations suggest whatever the right target was a decade ago, a higher target might be appropriate today given the slowdown in productivity and reduction in the neutral rate. Surely the risks of missing the target on the low side over a prolonged interval should be a major policy concern today.

This is a time of considerable financial and geopolitical fragility around the world. There are real risks of serious capital flight and associated dislocation in many emerging markets. Any change in policy and financial conditions carries with it at least some chance of setting off instability which could snowball given the current high degree of illiquidity in many markets. The risks are magnified by the asymmetry between what the Fed is doing and what most other major central banks are doing. While in principle exchange rate movements should not affect the level of global demand, further dollar appreciation is likely to be contractionary for the global economy because of the uncertainty it engenders.

On balance, the risks of raising rates seem a little more likely to play out and much more serious than the risks of standing still on rates. Moreover, given the inevitability of mistakes prudence dictates tilting towards making errors that are reversible. An excessive delay in raising rates can be remedied eight weeks later at the next FOMC meeting by raising them then. On the other hand, if rates are raised and it proves to be a mistake there are likely to be substantial costs as inflation expectations move down, financial turbulence ensues, and the economy possibly tips towards recession. Reversing the rate increase would be unlikely to eliminate these consequences. Moreover, reversing the direction of policy would hardly be helpful for central bank credibility as the central banks around the world who raised rates and then were forced to reverse themselves have discovered.

Reasonable people can come to different judgements on all of this. I think on balance it was a mistake to lock in a December rate increase though the argument is closer than it was in September. But that decision has been made. I hope the Fed will not now invest its credibility in signaling further increases until and unless there is much clearer evidence of accelerating inflation. I hope it will also emphasize the two sided character of the 2 percent inflation target to mitigate the risk that markets will think the U.S. has an inflation ceiling rather than target. Finally, I hope the Fed will signal its awareness of instability and risk of growing problems in emerging markets.

(FT) Central bankers do not have as many tools as they think

While debate about the relevance of the secular stagnation idea to current economic conditions continues to rage, there is now almost universal acceptance of a crucial part of the argument. It is agreed that the “neutral” interest rate, which neither boosts nor constrains growth, has declined substantially and is likely to be lower in the future than in the past throughout the industrial world because of a growing relative abundance of savings relative to investment.

The idea that real interest rates — that is, adjusted for inflation — will be lower than they have been historically is reflected in the pronouncements of policymakers such as Federal Reserve chair Janet Yellen, the medium-term forecasts of official agencies such as the Congressional Budget Office and the International Monetary Fund and the pricing of government bonds whose payments are tied to inflation.

This is important progress and has contributed to more prudent monetary policies than otherwise would have been made and the avoidance of a deflationary psychology taking hold particularly in Europe and Japan. Policymakers, despite having adjusted their views, still overestimate the extent to which neutral real interest rates will rise.

Neutral real interest rates may well rise over the next few years as the American economy creates jobs at a rapid rate and the effects of the financial crisis diminish. This is what many expect, though the fact that an imminent return towards historically normal interest has been widely expected for the past six years should invite scepticism.

A number of considerations make me doubt the US economy’s capacity to absorb significant increases in real rates over the next few years. First, they were trending down for 20 years before the crisis started and have continued that path since. Second, there is at least a significant risk that as the rest of the world struggles there will be substantial inflows of capital into the US leading to downward pressure on rates and upward pressure on the dollar, which in turn reduces demand for traded goods.

Third, the increases in demand achieved through low rates in recent years have come from pulling demand forward, resulting in lower levels of demand for the future. For example, lower rates have accelerated purchases of cars and other consumer durables and created apparent increases in wealth as asset prices inflate. In a sense, monetary easing has a narcotic aspect. To maintain a given level of stimulus requires continuing cuts in rates.

Fourth, profits are starting to turn down and regulatory pressure is inhibiting lending to small and medium sized businesses. Fifth, inflation mismeasurement may be growing as the share in the economy of items such as heathcare, where quality is hard to adjust for, grows. If so, apparent neutral real interest rates will decline even if there is no change in properly measured rates.

All of this leaves me far from confident that there is substantial scope for tightening in the US and there is probably even less scope in other parts of the industrialised world. The fact that central banks in countries, including Europe, Sweden and Israel, where rates were zero found themselves reversing course after raising rates adds to the cause for concern.

But there is a more profound worry. The experience of the US and others suggests that once a recovery is mature the odds of it ending within two years are about half and of it ending in less than three years over two-thirds. As normal growth is below 2 per cent rather than the historical near 3 per cent, the risk may even be greater. While recession risks may seem remote given rapid growth, no postwar recession has been predicted a year ahead by the Fed, the administration or the consensus forecast.

History suggests that when recession comes it is necessary to cut rates more than 300 basis points. I agree with the market that the odds are the Fed will not be able to raise rates100 basis points a year without threatening to undermine recovery. Even if this were possible, the chances are very high that recession will come before there is room to cut rates enough to offset it. The knowledge that this is the case must surely reduce confidence and inhibit demand.

Central bankers bravely assert that they can always use unconventional tools. But there may be less in the cupboard than they suppose. The efficacy of further quantitative easing in an environment of well-functioning markets and already very low medium-term rates is highly questionable. There are severe limits on how negative rates can become. A central bank forced back to the zero lower bound is not likely to have great credibility if it engages in forward guidance.

The Fed will in all likelihood raise rates this month. Markets will focus on the pace of its tightening. I hope their response will involve no great turbulence. But the unresolved question that will hang over the economy is how policy can delay and ultimately contain the next recession. It demands urgent attention from fiscal as well as monetary policymakers.

(FT) Foreign exchange shift drives US and euro equity performance

Latest job numbers give Fed leeway to tighten rates this month — if it so chooses

December 5, 2015by: John Authers

What a long strange trip it’s been. The year is almost over. Its biggest event as far as markets are concerned — the first rise in US target interest rates in almost a decade — is still ahead, but now seems a virtual racing certainty.

Key markets are on course to end 2015 roughly as was expected, and much in line with each other. The route to get here, however, has been surprising. And it has required some huge shifts in foreign exchange markets.

At the outset of 2015, there was a cosy consensus that the Federal Reserve would start to raise rates, and that the European Central Bank, far more reluctant to resort to easy money, would be obliged to resort to unorthodox measures to jolt life into its economy.

Indeed, as the year ends, two-year government yields — highly sensitive to interest rate expectations — in the US have gained about a quarter of a percentage point (to 0.93 per cent) and in Germany have lost about a quarter of a percentage point (to the stunningly low level of minus 0.3 per cent). The Fed, following the broadly positive US employment report for November on Friday, is almost certain to raise rates this month. The ECB, as confirmed on Thursday, has cut rates, resorted to quantitative easing, and then extended QE.

For stock markets, as the chart shows, the German and US markets are almost exactly where they started the year, and identical with each other, in dollar term performance. On the key questions of interest rates in the main developed economies, and of equities, 2015 has seen a steady and small adjustment.

But that does not account for all that happened in between. At the year’s outset, many thought the Fed would be well into its tightening cycle by now. Two months ago, after the summer panic over China, all thought of a rate rise this year had been abandoned. European equities were poised for more impressive gains, before the China crisis, the midsummer imbroglio over Greece, the Volkswagen scandal and some dreadful corporate profit numbers cut them back down to size.

Also, of course, it ignores the currency effect, which has played a critical balancing role as the world tries to resolve its divergences. The dollar has strengthened by almost 9 per cent for the year. It had gained about 11 per cent before the extraordinary events of Thursday, when disappointment at the ECB’s announcement on QE led to the second-strongest daily gain for the euro against the dollar in its history.

The gentle adjustment has happened, but only after some huge moves in currencies, and some epic misunderstandings as central banks attempt to communicate their plans to markets.

What are the key points? First, the world economy is not very exciting at present, however it is spun. China’s growth is slower than it was. Europe’s flirtation with disaster over Greece did nothing to lift the gloom, even if things appear to be improving a little at the end of the year. In the US, even if the unemployment rate is stabilising at a historically acceptable rate, the rate of improvement has stalled, and the figures are flattered by the historically high numbers who have abandoned attempts to find work. The manufacturing sector is slumping, and the economy is reliant for growth on services, where employment is more volatile.

The latest employment numbers left the way open for the Fed to tighten rates this month as it wishes. They did not prompt any great excitement.

Secondly, money is fungible, and investors’ confidence is still so weak that they require regular new doses of it from central banks. The S&P 500 went negative for the year on Thursday in the wake of the ECB disappointment, because traders had been banking that some of the money injected into Europe would cross the Atlantic. That the US market has stayed so close to its record high set in May, despite likely Fed tightening, was largely because of expected infusions from other central banks.

Third, expectations matter. The second greatest daily appreciation of the euro in its history came on a day when the ECB cut rates and extended QE — a move that should unambiguously weaken the currency by making it less attractive for foreigners to park funds there. For context, the only day when the euro rose more against the dollar came in 2009 when it was the Fed that resorted to QE.

As with some of the year’s other big market switchbacks, such as China’s unheralded currency devaluation, the move was driven by investors’ surprise. Mario Draghi has a history of surprising investors when he wants to make a point. The package he announced on Thursday was radical — but investors had placed big bets on his cutting rates by even more, and on his expanding monthly bond purchases, rather than merely extending the period over which they would continue.

It has taken Sturm und Drang, some huge misunderstandings and a big shift in the foreign exchange market to engineer even the modest divergence in monetary policy that 2015 now seems set to deliver. It is as well to brace for volatility to continue, and to intensify.